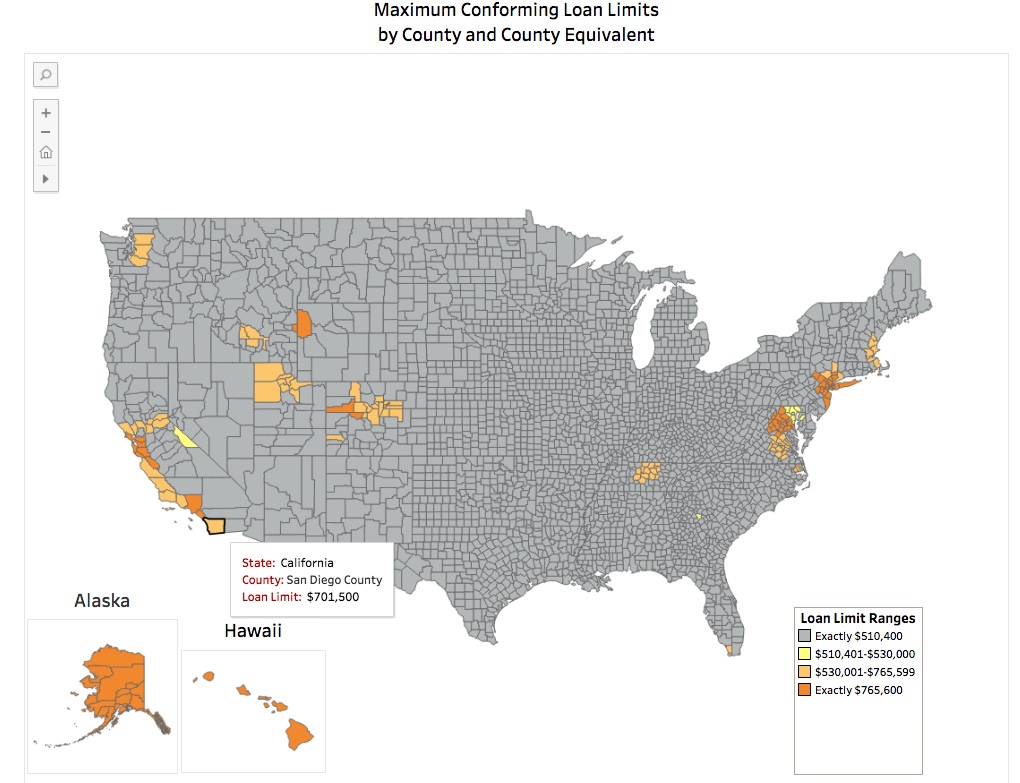

Just before the end of November, the Federal Housing Finance Agency (FHFA) announced new maximums for 2020 conforming loan limits on mortgages that will be acquired by Fannie Mae and Freddie Mac. For one-unit properties nationwide, the maximum limit increased to $510,400 – a 5.38 percent rise from the $484,530 number from this year. This makes it the fourth consecutive year that the FHFA has increased limits. The new change will apply to the majority of counties, except for 43 – all over the country.

What does this mean? In short, what exciting news for homebuyers and sellers! Those looking to take advantage of these limits also don’t have to wait until January. Some lenders will be able to start funding with the new loan limits right away.

To get a better understanding of these new loan limits, see below for specific numbers and how that might help you. Each county and state is different. Make sure to check out local numbers to find out more information.

Conforming (or Baseline) Loan Limit

After evaluating the median home prices, metro and economic stats, the Federal set a new maximum. The FHFA showed in a recent report how the Housing Price Index plays a significant role in the limit adjustments. They found that home prices rose for 33 quarters in a row in the U.S., and just this last quarter there was a 4.9 percent difference from 2018’s third quarter with prices rising in every state. On average, there was an average 5.5 percent rise in states with the top and lowest annual appreciation. Therefore, conforming loan limits match a similar increase.

Increased loan limits allow more consumers the opportunity to choose between more homes. With a $26,000 increase, buyers will have more room to put down less money upfront and still be eligible to get a conforming loan. Ultimately, buyers can get more, bigger homes, for their money. This is great for sellers who are considering putting their house on the market. There’s the availability to go to a 5 to 10 percent increased listing amount and still have their home be available for more buyers without them having to follow Jumbo Loan guidelines.

High-Balance

Loan limits for high-balanced areas have also risen due to the increase of the median home prices this year. Think of areas such as New York City, Los Angeles or the Orange County areas, San Francisco, and Washington D.C. Places are considered “high-cost” if 115 percent of the local median home value exceeds that new set conforming loan limit. The FHFA jumped this number to $765,600 from $726,525. That’s almost an additional $40,000 which is 150 percent more than the conforming, baseline limit. This creates a ‘ceiling’ giving room for the higher cost of living for buyers in that area.

For example, like many coastal California counties, San Diego County’s limit will sit on a higher-end at a $701,500 limit, while others reach up to that max $765,600 limit.

FHA and VA Loans

Not long after the initial FHFA announcement, the FHA followed close behind with new limits early December. The baseline limit for FHA is 65 percent of the national conforming loan limit amount. Since the FHFA raised the new limit to $510,400, this makes the new FHA Loan at $331,760 and applies for most of the lower-cost areas in the country. These new FHA loan limits will be applied to single-units and up to four-units. Housing Wire included some history of the FHA loan limit behaviors:

Back in 2016, the FHA increased loan limits for just 188 counties; in 2017, this number jumped to 2,948 counties; then to 3,011 counties for 2018. In 2019, the FHA loan limits increased in 3,053 counties.

Interestingly enough, some FHA limits will decrease – some by almost 50 percent. FHA showed that there are 11 counties, including some in New York State, North Caroline, Texas and Tennessee specifically due to price changes.

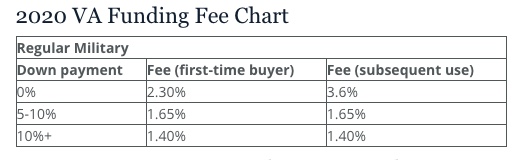

For the VA loan, buyers can put as little as 0 percent down as there is neither a down payment nor mortgage insurance required. Over the summer 2019, VA loan limits were eliminated. The numbers will still be based on location and county, but there will no longer be a set max limit.

When using a VA loan, there is a funding fee. Depending on your circumstance, this fee will cover the mortgage insurance and is due at closing. For 2020, that fee will rise .15 percent from 2.15 to 2.30 percent. See the chart below for the different fee changes:

Overall, this will be a great way to kick off the new year, for buyers, sellers, and industry professionals. Homeowners can also use these new numbers to their benefit. There will be more room to refinance current loans, renovate homes, consolidate any high-cost debt, and save more money each month.

If you’re interested in learning more about these new loan limits, give my office a call. I’d love to see how we can help!

This article is intended to be accurate, but the information is not guaranteed. Please reach out to us directly if you have any specific real estate or mortgage questions or would like help from a local professional. The article was written by Sparkling Marketing, Inc. with information from resources like FHFA, and Housing Wire.